Waiting It Out Is Making It Worse: The Real Cost of Stalling on an Emergency Loan

There's a particular kind of denial that kicks in when money gets tight. You know the bill is sitting on the counter. You know the account balance isn't going to magically recover overnight. But something in your brain decides that if you just don't look at it directly — if you give it a few more days — maybe the situation will sort itself out.

It won't. And the longer you wait, the more it costs.

This isn't about scaring you into a decision. It's about getting honest about what procrastination actually does to your finances when you're already in crisis mode. Because "I'll figure it out later" isn't a plan — it's a penalty fee waiting to happen.

The Snowball Nobody Talks About

Financial emergencies don't stay the same size. They grow. Every day that passes without a resolution adds friction — in the form of late fees, interest, shutoff charges, and compounding penalties — that makes the original problem harder to solve.

Think about it this way: a $400 shortfall on rent on the 1st of the month doesn't stay at $400 if you ignore it. By the 5th, you might be looking at a $50 late fee. By the 10th, your landlord may have initiated the first steps of a formal notice. By the 30th, you're dealing with potential eviction proceedings that carry legal and administrative costs — not to mention the credit damage that follows.

What could have been solved with a fast personal loan on day one has now become a multi-layered crisis with consequences that stretch weeks or months into the future.

Real Scenarios, Real Dollar Costs

The Missed Car Payment

Let's say your car payment of $380 is due on the 15th and you're $300 short. You tell yourself you'll catch up when your next paycheck hits in two weeks.

Here's what actually happens:

- Day 1–10: Most lenders offer a grace period, but the clock is running.

- Day 11–30: A late fee of $25–$50 gets added. Your credit score may take a hit if the lender reports to the bureaus after 30 days.

- Day 31+: You're now officially 30 days late. That mark on your credit report can lower your score by 60–110 points depending on your current standing — affecting your ability to get future credit at reasonable rates.

- Day 60–90: Repossession becomes a real possibility. Repo fees alone can run $200–$500, and you'll still owe the remaining balance on the loan.

That $300 gap you thought you'd bridge "next paycheck" has now triggered a chain reaction with consequences that outlast the original emergency by months.

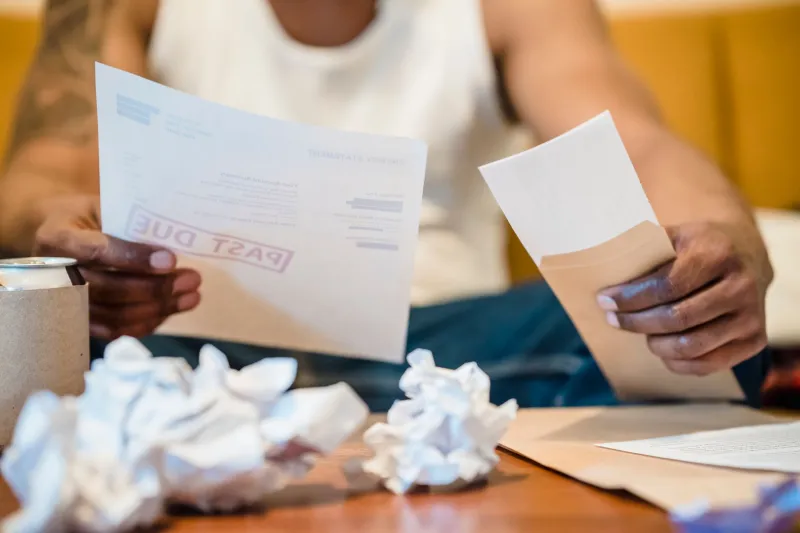

The Surprise Medical Bill

You get a bill for $650 from an out-of-network provider after a visit to urgent care. You don't have the cash right now, so you set it aside to deal with later.

Medical billing works differently than most people realize. After 60–90 days, unpaid medical bills are often sent to collections. Once that happens:

- Your credit report takes a hit that can linger for years.

- The collections agency may add fees on top of the original balance.

- Negotiating the original bill — which is often possible if you contact the provider early — becomes much harder once it's been handed off.

Acting within the first two to three weeks gives you leverage. Waiting strips it away.

The Overdue Utility Notice

You're $180 behind on your electric bill. You figure you'll pay it when things loosen up a bit. Then the shutoff notice arrives.

Utility reconnection fees typically run $50–$200 depending on your provider and state. Some utilities also require a deposit before restoring service if you've had a shutoff — sometimes equal to two months of your average bill. So that $180 you owed has now turned into $180 + $100 reconnection fee + potentially $300–$400 in deposit requirements before your lights come back on.

The math is brutal. And it's entirely avoidable.

Why People Stall — And Why It Makes Sense (Until It Doesn't)

It's worth being honest about why the delay happens in the first place. It's not stupidity or laziness. It's a very human response to stress.

When we're overwhelmed, our brains default to avoidance. Looking at the problem head-on feels worse in the short term than looking away. There's also a common misconception that applying for a loan is complicated, slow, or likely to end in rejection — so why bother?

But here's the reality in 2025: emergency personal loan applications through online lenders like XpressLoans 911 take minutes, not days. Approvals can come back fast. And funds can hit your account far sooner than most people expect.

The barrier is mostly psychological. The actual process? Much more straightforward than the anxiety around it suggests.

The Empowering Flip Side: What Early Action Buys You

When you address a financial emergency head-on — especially within the first 24 to 48 hours — you're working with options, not against consequences.

You can:

- Pay before late fees kick in, keeping the total you owe as small as possible.

- Protect your credit score, avoiding the 30-day mark that triggers bureau reporting.

- Negotiate from a position of strength, since creditors and landlords are far more flexible when you're proactive.

- Stop the compounding cycle before it has a chance to start.

A short-term personal loan used strategically isn't a sign that you've failed financially. It's a tool — one that, when deployed quickly, can actually cost you less than the alternative of waiting.

A Simple Way to Think About It

Next time you're tempted to delay, ask yourself one question: What does this problem look like in 30 days if I do nothing?

Walk through it honestly. Add up the late fees, the potential credit damage, the reconnection costs, the snowballing penalties. Then compare that number to what it would cost to address it today with a fast personal loan.

In most cases, the math isn't close.

Emergency loans exist precisely for moments like this — not as a last resort after everything has already gone sideways, but as a fast, practical response that keeps a manageable problem from becoming an unmanageable one.

The Bottom Line

"I'll figure it out later" feels like patience. In a financial emergency, it's actually procrastination with a price tag attached.

The good news? Acting fast is easier than it's ever been. If you're staring down a bill, a payment, or a shortfall right now, the smartest move is also the simplest one: find out what you qualify for before the clock runs out. At XpressLoans 911, that process starts in minutes — because when money is tight, time is the one thing you really can't afford to waste.