Doing Nothing Is Still a Decision: The Hidden Cost of Waiting on an Emergency Loan

There's a story a lot of us tell ourselves when money gets tight: I'll figure it out. Maybe the paycheck will stretch further than expected. Maybe a friend comes through. Maybe the bill collector gives you a little grace. It's a comforting story — and for a lot of people, it's the reason a manageable problem quietly becomes a financial disaster.

Here's the uncomfortable truth: choosing to wait is still choosing. And in most financial emergencies, waiting is one of the most expensive options on the table.

The Psychology Behind Financial Avoidance

When something feels overwhelming, the brain's default move is often to pull back. Psychologists call it avoidance behavior — we delay decisions that feel uncomfortable or uncertain, even when acting would clearly be better for us. With money, this shows up constantly. We don't open the bill. We don't call the lender. We don't look at the bank balance.

And we definitely don't apply for a loan, because that feels like admitting things are bad.

But here's the thing: things are already bad. You didn't make them bad by acknowledging it. The overdue electric bill exists whether you open the envelope or not. The overdraft fee hits whether you log into your account or not. Avoidance doesn't pause the problem — it just takes you out of the driver's seat while the problem keeps moving.

Applying for an emergency loan isn't a white flag. It's a strategic move. It's you deciding to engage with the situation instead of hoping it resolves itself.

Real Dollars, Real Delays: What 'Waiting to See' Actually Costs

Let's get specific, because the math here is pretty eye-opening.

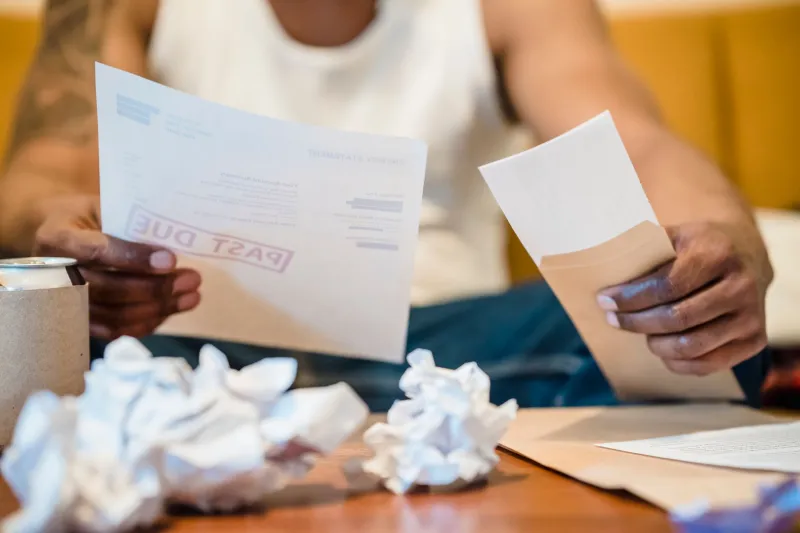

The Utility Disconnect Spiral

Say your electric bill is $180 past due. You're telling yourself you'll catch it next week. But next week, the power gets shut off. Now you're not looking at $180 — you're looking at $180 plus a $50 late fee, plus a $75–$200 reconnection fee depending on your utility provider, plus maybe a deposit requirement if your account history looks shaky. That's potentially $400+ to solve a $180 problem. The delay didn't save you anything. It cost you more than twice the original amount.

The Overdraft Spiral

You've got $12 in your checking account and a $300 car insurance payment due tomorrow. You figure you'll deal with it after payday — four days away. But a subscription auto-renews. Then a small charge hits. Suddenly you've got three overdraft fees at $35 each. That's $105 in penalties on top of the original shortfall. Some banks will even charge extended overdraft fees if you stay negative for more than a few days. A single week of avoidance just cost you over a hundred bucks in pure penalties.

The Late Fee Compounding Effect

Credit cards are notorious for this. Miss a payment, and you're hit with a late fee — often $30 to $40. Your interest rate might jump to a penalty APR that can top 29%. Now the balance you were already struggling with is growing faster, and your minimum payment just went up. What started as a cash flow hiccup is turning into a debt that takes months to unwind. The longer you wait to stabilize your finances, the longer that penalty APR eats at you.

The Rental or Housing Risk

Fall behind on rent, even by a few weeks, and you're not just risking a late fee — you're risking a formal notice, a mark on your rental history, and in some states, the start of an eviction process that can follow you for years. Landlords can move fast. What felt like a short-term cash crunch can turn into a long-term housing problem if you wait too long to address the gap.

'But I Don't Want to Take on Debt'

Fair. Nobody does. But let's reframe the comparison.

You're not choosing between debt and no debt. You're choosing between controlled debt — a personal loan with a known rate, a fixed term, and a clear payoff date — and uncontrolled debt — penalty fees, compounding interest, service interruptions, and the kind of financial chaos that tends to snowball.

A fast personal loan through a service like XpressLoans 911 gives you something that late fees and overdrafts never will: predictability. You know what you're borrowing. You know what you're paying back. You have a plan. That's not a last resort — that's financial management.

Why Speed Actually Matters Here

Not all debt is created equal, and not all timing is either. Emergency loans are specifically designed for situations where the cost of delay exceeds the cost of borrowing. That's not a marketing line — it's the math we just walked through above.

The faster you act, the more of the damage you can cut off before it compounds. That $180 utility bill is a much cleaner problem to solve than the $400 reconnection situation it becomes five days later. Getting funded today — before the overdraft hits, before the notice goes out, before the penalty APR kicks in — is almost always cheaper than getting funded next week.

XpressLoans 911 is built around that reality. Fast applications, quick decisions, and funding that can hit your account without the multi-week bank timeline that makes emergency loans feel pointless. When the emergency is now, the solution needs to be now too.

Taking Control Is the Move

There's no version of financial avoidance that ends with the problem quietly going away. Bills don't forget. Lenders don't forget. Utility companies definitely don't forget. What they do is charge you for the wait.

If you're in the middle of a financial crunch right now and you've been telling yourself you'll figure it out later — this is the moment to ask: what is later actually costing me? Run the numbers. Add up the late fees, the penalties, the potential reconnection costs, the overdraft charges. Then compare that to the cost of borrowing what you need today.

For most people in a genuine emergency, the math isn't even close.

Acting now isn't panic. It's not giving up. It's recognizing that inaction is already a financial decision — and choosing to make a better one.