Small Problem, Bigger Disaster: How Putting Off a Financial Emergency Turns $800 Into $2,500

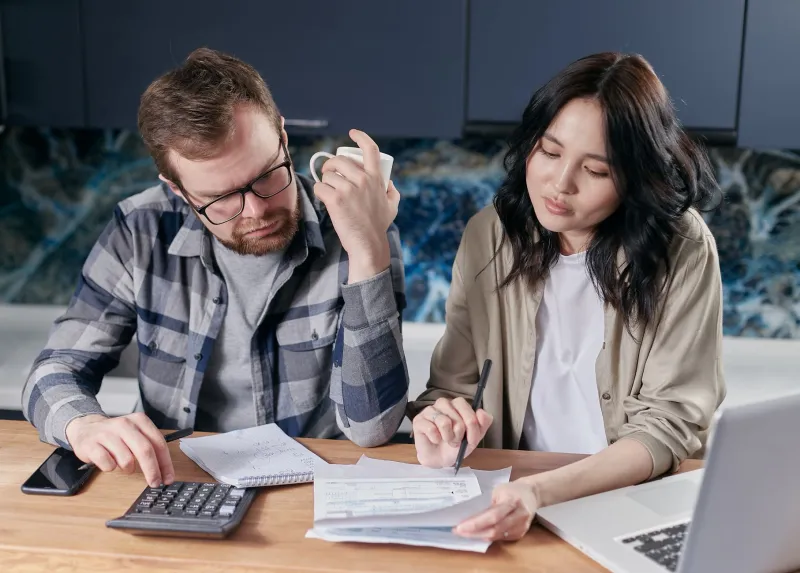

There's a very human instinct that kicks in when money trouble shows up at the door. Instead of answering it, a lot of us just... don't. We tell ourselves we'll figure it out after the weekend, after payday, after things settle down a little. It feels like patience. It feels responsible, even — like we're not rushing into anything.

It's not patience. It's a trap.

The 'I'll figure it out later' mindset is one of the most financially damaging habits people fall into during a crisis — not because the original problem is so catastrophic, but because waiting quietly transforms a manageable situation into a full-blown disaster. The numbers don't stay frozen while you think it over. They grow.

The Psychology Behind the Delay

Psychologists call it present bias — our tendency to prioritize immediate comfort over future consequences. When a bill hits that you can't immediately cover, the stress of confronting it feels worse in the moment than the vague, future pain of letting it slide. So you slide.

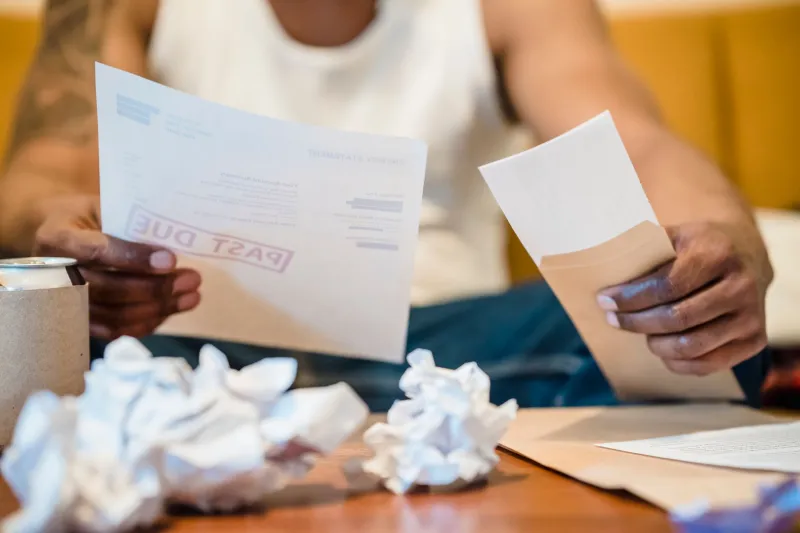

But here's the thing about financial emergencies specifically: they don't respond to being ignored the way other problems might. A difficult conversation might cool down if you wait. A financial shortfall? It compounds. Late fees get added. Interest kicks in. Accounts go to collections. Credit scores dip. And suddenly, the $800 problem you were avoiding has a $2,500 price tag.

Let's look at exactly how that happens in the real world.

Scenario 1: The Missed Rent Payment

You're $750 short on rent this month. You figure you'll catch up next paycheck — two weeks away. No big deal, right?

Except your lease has a standard late fee clause: 5% after five days. That's $37.50 on day six. Some leases charge daily fees after that. Your landlord, now irritated, starts the formal notice process. In many states, that means a written notice to pay or vacate — and if you don't resolve it quickly, you're looking at an eviction filing.

Eviction filings show up on rental history reports. Even if you eventually pay and avoid being removed, that filing can follow you for years, making it significantly harder to rent again. What started as a short-term cash gap has now threatened your housing stability and your rental record.

A fast personal loan covering that $750 on day one? That's the version of this story where nothing else goes wrong.

Scenario 2: The Car That Needs to Run

Your mechanic tells you the repair is $900. You don't have it right now, so you decide to limp the car along for a few more weeks and hope for the best.

Two weeks later, the original issue — let's say a failing water pump — has caused the engine to overheat twice. Now you're looking at potential head gasket damage. That $900 fix just became a $2,200 repair. Or worse, the car is totaled and you're suddenly without transportation entirely.

For anyone who drives to work, losing a vehicle isn't just inconvenient — it can mean losing income. Rideshare costs, missed shifts, or even a job loss can follow. The ripple effect from one postponed repair is genuinely staggering when you map it out.

Scenario 3: The Medical Copay You Skipped

You've got a health issue that needs attention, but the copay and potential prescription costs feel like too much right now. You'll go next month when things are better financially.

Next month, the condition has worsened. Now you need a specialist referral, additional testing, and possibly a more aggressive treatment plan. What might have been a $150 copay and a $40 prescription is now a series of appointments, higher-tier copays, and potentially lost workdays.

Beyond the physical toll, unpaid medical bills that eventually go to collections are one of the leading causes of credit score damage in the US. Millions of Americans have a medical debt dragging down their credit right now — often from a bill they meant to handle 'later.'

The Hidden Multiplier: Your Credit Score

One of the sneakiest ways delay makes things worse is through your credit score. Miss a payment by 30 days? That's potentially a 60 to 110 point drop, depending on your credit history. Once a missed payment hits your report, it stays there for seven years.

A lower credit score means higher interest rates on future borrowing — every loan, every credit card, every car financing deal becomes more expensive. The cost of that one moment of delay compounds across every financial decision you make for years afterward.

Compare that to taking out a short-term personal loan to cover the gap: yes, there's interest involved. But you're paying a known, fixed cost to stop the bleeding — rather than letting an unknown, escalating cost run wild.

Why a Fast Personal Loan Is the Proactive Move

There's a misconception that borrowing money during a crisis is a sign of financial weakness or poor planning. That's worth pushing back on.

Using a fast personal loan to handle a real emergency isn't reactive — it's strategic. You're making a calculated decision to contain the damage at a known cost, before it grows into something far harder to manage. That's not panic borrowing. That's financial triage.

At XpressLoans 911, the whole point is to get you access to emergency cash quickly — because we understand that the window between 'manageable problem' and 'full crisis' can close fast. When your car won't start Monday morning, when rent is due Friday, when a medical bill is heading to collections, speed matters.

The application process is straightforward, approval can happen fast, and funds can hit your account when you actually need them — not after the damage is already done.

Stop Negotiating With the Problem

Here's the honest truth: most people who delay dealing with a financial emergency aren't lazy or irresponsible. They're overwhelmed, and avoidance feels like relief. But the relief is temporary. The consequences aren't.

If you're sitting on a financial problem right now — a bill past due, a repair you've been putting off, a payment you've been hoping will somehow resolve itself — ask yourself one question: what does this cost me if I wait another two weeks?

For most real emergencies, the answer is: more than you want to pay.

The 'figure it out later' version of you is borrowing against the future. The version of you that acts today gets to keep more of it.